Sharlene Tullao

Transforming

Financial Challenges

into Opportunities for Generational Change.

Tax-Free Strategy Solution / Retirement Income Planning / Transfer Your Legacy / Business Succession Planning / Living Benefits / Index Strategy

The Hidden Retirement Risks You Can’t Afford to Ignore

Get this free guide and discover the insider strategies the top 1% use to protect their money — without the risk, fees, or tax surprises. Whether you’re close to retirement or already there, this checklist will help you spot hidden traps and keep more of what you’ve earned.

Practical. Insightful. Transformative. And yes — it’s completely free.

👉 Download your guide now and start building a stronger, smarter retirement plan.

AS SEEN ON:

Sharlene Tullao

Transforming

Financial Challenges

into Opportunities for Generational Change.

Tax-Free Strategy Solution / Retirement Income Planning / Transfer Your Legacy/ Business Succession Planning / Living Benefits / Index Strategy

Tax-Free Strategy Solution / Retirement Income Planning / Transfer Your Legacy

Business Succession Planning / Living Benefits / Index Strategy

The Hidden Retirement Risks You Can’t Afford to Ignore

Get this free guide and discover the insider strategies the top 1% use to protect their money — without the risk, fees, or tax surprises. Whether you’re close to retirement or already there, this checklist will help you spot hidden traps and keep more of what you’ve earned.

Practical. Insightful. Transformative. And yes — it’s completely free.

👉 Download your guide now and start building a stronger, smarter retirement plan.

AS SEEN ON:

Why Choose Us

Why Choose Us

Understand Your Money,

Own Your Future.

With easy-to-understand tips and personalized strategies, we help you ditch the confusing jargon, dodge those sneaky

fees and taxes, and build real wealth—so you can live well, give more, and leave a legacy that lasts.

Ready to take control of your financial future? Let’s chat! and let’s turn your money goals into a game plan.

With easy-to-understand tips and personalized strategies, we help you ditch the confusing jargon, dodge those sneaky fees and taxes, and build real wealth—so you can live well, give more, and leave a legacy that lasts.

Ready to take control of your financial future? Let’s chat! and let’s turn your money goals into a game plan.

Imagine a better way.

Grow it. Protect it. Control it. Your money, your way — with flexibility and security.

Traditional

Approach

Tax-Deferred: Pay taxes later — at unknown future rates

Market Risk: Fully exposed to market ups and downs

High Fees: 1–2% management fees draining your returns every year

Limited Access: Early withdrawal penalties lock up your money

One-Size-Fits-All: Generic advice from cookie-cutter group plans

Strategic Approach

(Our Method)

Tax-Free Growth & Access: Keep more of what you earn

Principal Protection: Safeguard your money from market losses

Zero Fees: No advisory or management fees eating into returns

Full Liquidity: Access your money anytime — no age restrictions

Designed for You: Aligned with your habits, ability, and time frame

WHAT YOU GET

✅ Security & Growth: Your money grows steadily, shielded from market chaos and free from Wall Street’s grip.

✅ Predictable Freedom: Enjoy a reliable, tax-free income you can count on for life — month after month, year after year.

✅ Confidence & Lifestyle: Live with peace of mind, knowing your future is secure, your legacy is preserved, and you’re free to travel, give, and fully enjoy life without financial fear.

About

Sharlene Tullao

Sharlene Tullao is more than a financial strategist—she is a catalyst for change, helping individuals transform financial uncertainty into opportunities for growth and security. Her journey began in client service and administrative roles, where she developed strong communication and problem-solving skills, learning to build meaningful relationships and navigate complex financial situations.

Determined to make a difference, she leveraged her understanding and experience in banking, mortgages, insurance, and investments to help clients navigate their finances with confidence. Guided by three core values—empowerment, integrity, and innovation. Sharlene ensures that individuals and families have the knowledge and tools needed to build lasting financial security.

More than just managing numbers, her mission is to provide guidance and direction so clients can achieve long-term wealth and peace of mind. She takes pride in fostering trust and collaboration, ensuring her clients feel supported every step of the way.

Our Services

Tax-Free Strategy Solution

Discuss the significance of Tax Advantaged Solutions at different life stages.

The top 1% plan and invest differently and it’s not by chance. These time-tested strategies have long been used by the well-informed and high earners, but the truth is, you don’t need to be wealthy to access them. Most advisors don’t share these approaches because their either not licensed, trained, or incentivized to do so. As a result, many people unknowingly rely on guidance that chips away at their future- often losing a decade or more of retirement income to hidden fees.

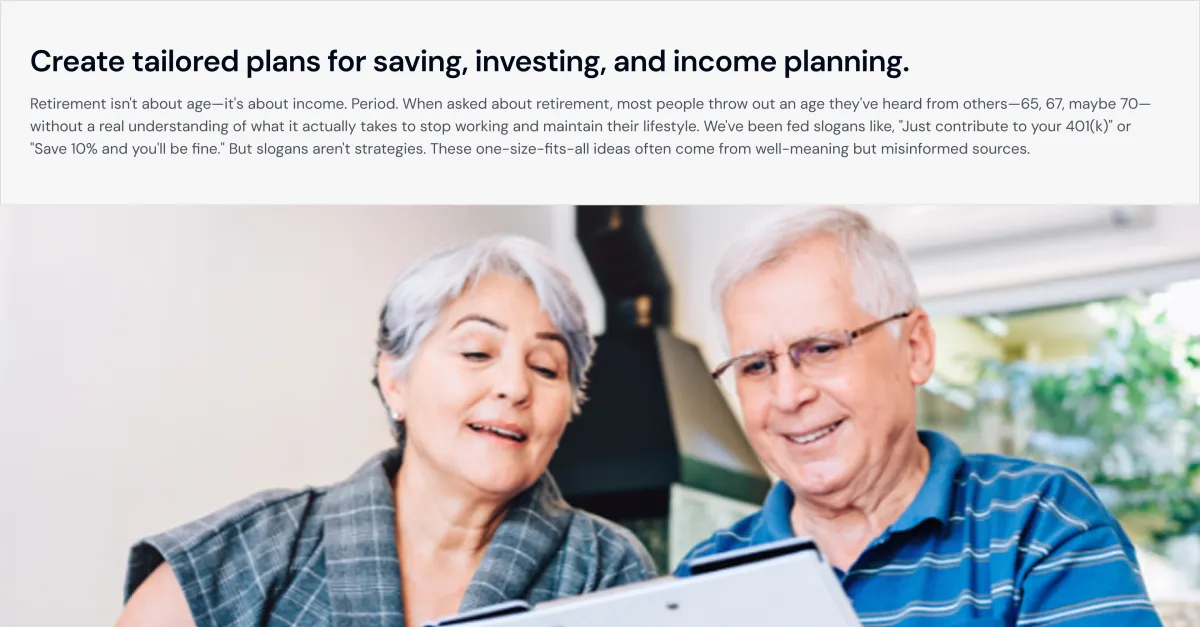

Retirement Income Planning

Create tailored plans for saving, investing, and income planning.

Retirement isn't about age—it's about income. Period. When asked about retirement, most people throw out an age they've heard from others—65, 67, maybe 70—without a real understanding of what it actually takes to stop working and maintain their lifestyle. We've been fed slogans like, "Just contribute to your 401(k)" or "Save 10% and you'll be fine." But slogans aren't strategies. These one-size-fits-all ideas often come from well-meaning but misinformed sources.

Transfer Your Legacy

Plan and protect your legacy with wills and trusts to safeguard assets and pass on your wishes to future generation.

At some point, we'll all face the reality of passing on—but what we leave behind can make all the difference. Legacy planning isn't just for the wealthy; it's for anyone who cares about their family's future. While it's uncomfortable to think about mortality, having a plan in place removes the stress of "what if" and gives you peace of mind, knowing your loved ones will be protected. Too often, people delay these decisions, not realizing the lasting impact they can make by acting now.

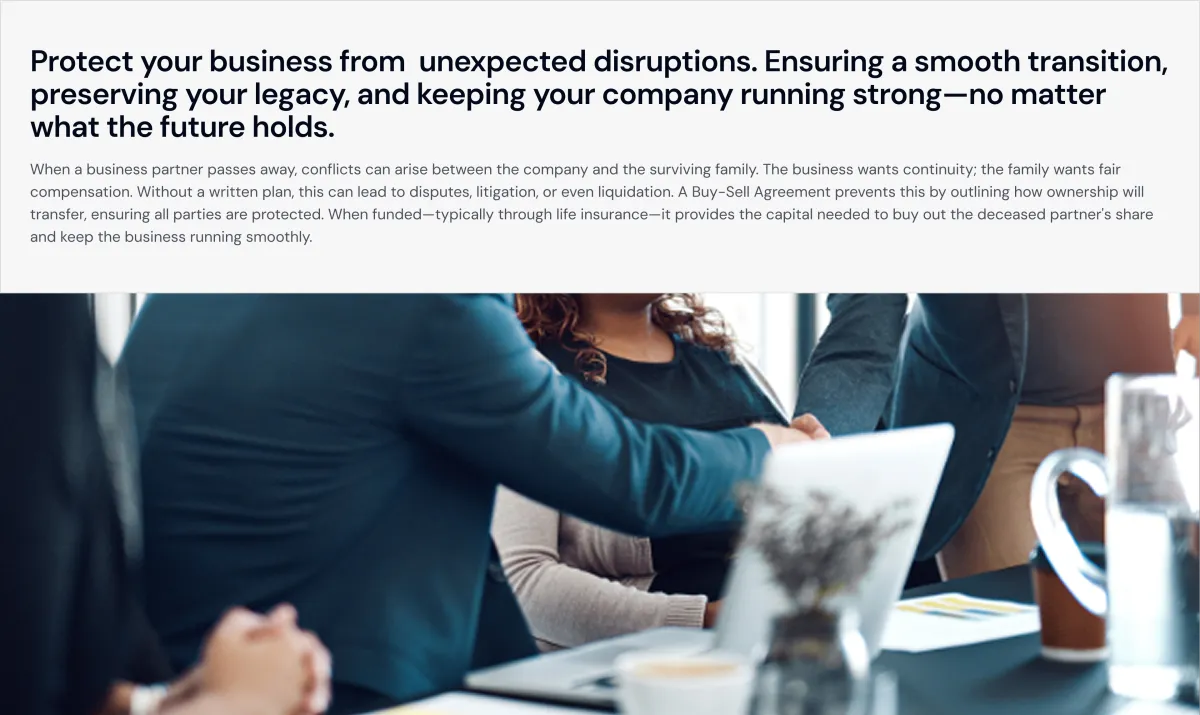

Business Succession Planning

Protect your business from unexpected disruptions. Ensuring a smooth transition, preserving your legacy, and keeping your company running strong—no matter what the future holds.

When a business partner passes away, conflicts can arise between the company and the surviving family. The business wants continuity; the family wants fair compensation. Without a written plan, this can lead to disputes, litigation, or even liquidation. A Buy-Sell Agreement prevents this by outlining how ownership will transfer, ensuring all parties are protected. When funded—typically through life insurance—it provides the capital needed to buy out the deceased partner's share and keep the business running smoothly.

Living Benefits

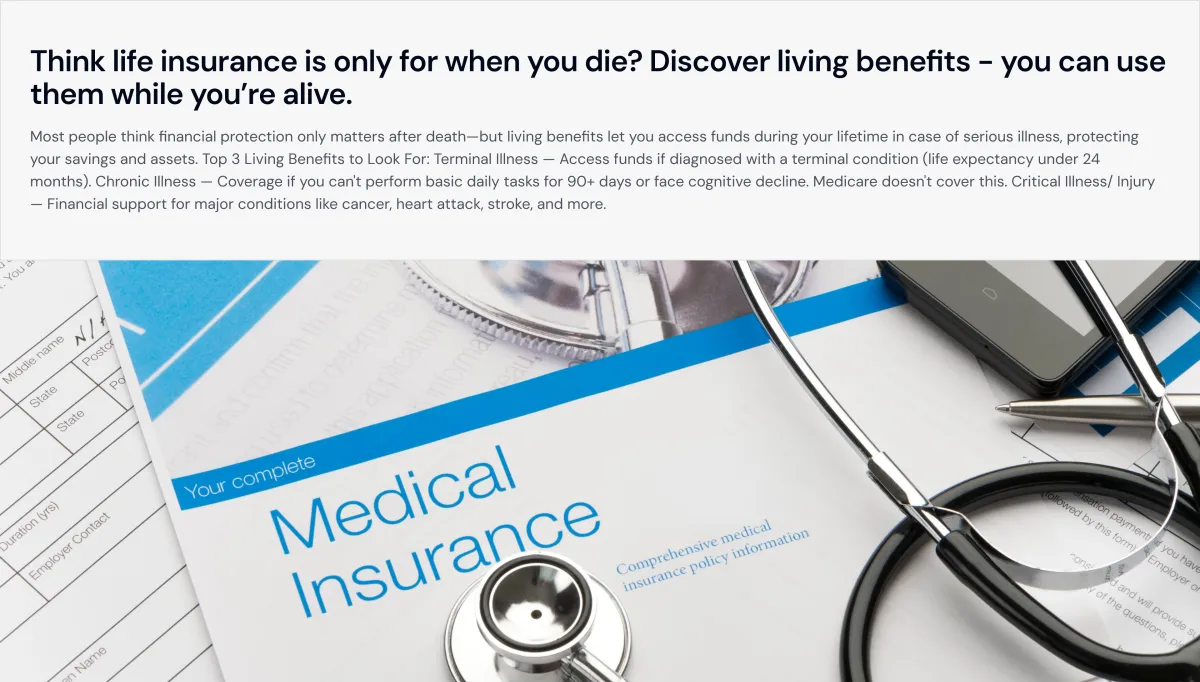

Think life insurance is only for when you die? Discover living benefits - you can use them while you’re alive.

Most people think financial protection only matters after death—but living benefits let you access funds during your lifetime in case of serious illness, protecting your savings and assets. Top 3 Living Benefits to Look For: Terminal Illness — Access funds if diagnosed with a terminal condition (life expectancy under 24 months). Chronic Illness — Coverage if you can't perform basic daily tasks for 90+ days or face cognitive decline. Medicare doesn't cover this. Critical Illness/ Injury — Financial support for major conditions like cancer, heart attack, stroke, and more.

Index Strategy

Key Benefits:

• Principal protection from market losses Tax-free growth and access

• No penalties, restrictions, or age requirements

• Full liquidity and flexible use of funds

• No advisor or management fees eating into your savings

• Greater peace of mind for your future and retirement

An indexed strategy lets you grow your money based on the performance of a market index— without exposure to market risk or volatility. Your funds aren't in the market, they're linked to it, offering the potential for growth with built-in protection. Top institutions in the U.S. use these strategies, linked to well-known indices like the S&P 500, Global Index, Fidelity Multifactor Yield 5% ER, Barclays Trailblazer Sector 5, and Credit Suisse Balanced Trend 5%, among others.

Our Services

What We Offer

Tax-Free Strategy Solution

Retirement Income Planning

Transfer Your Legacy

Business Succession Planning

Living Benefits

Index Strategy

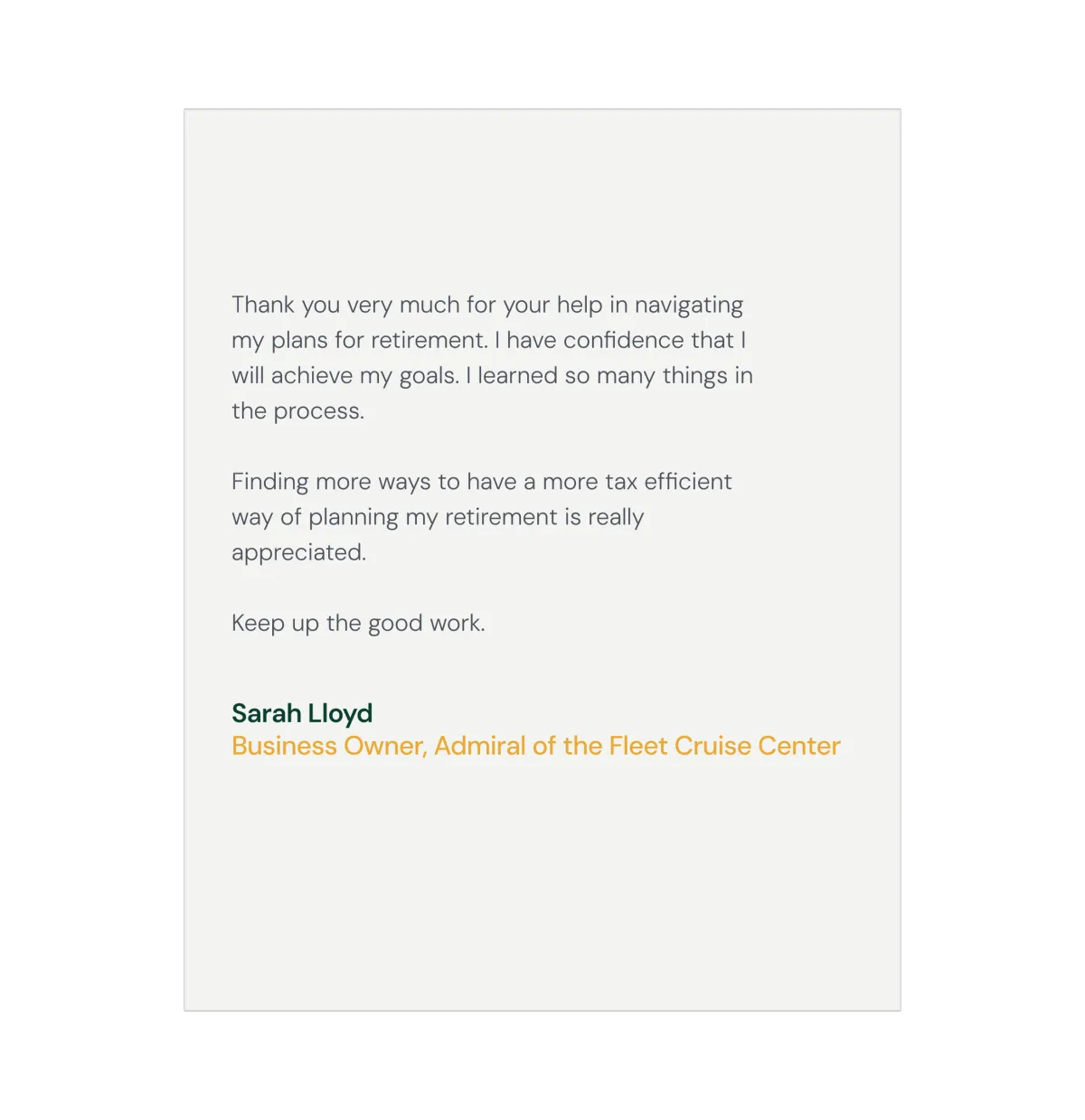

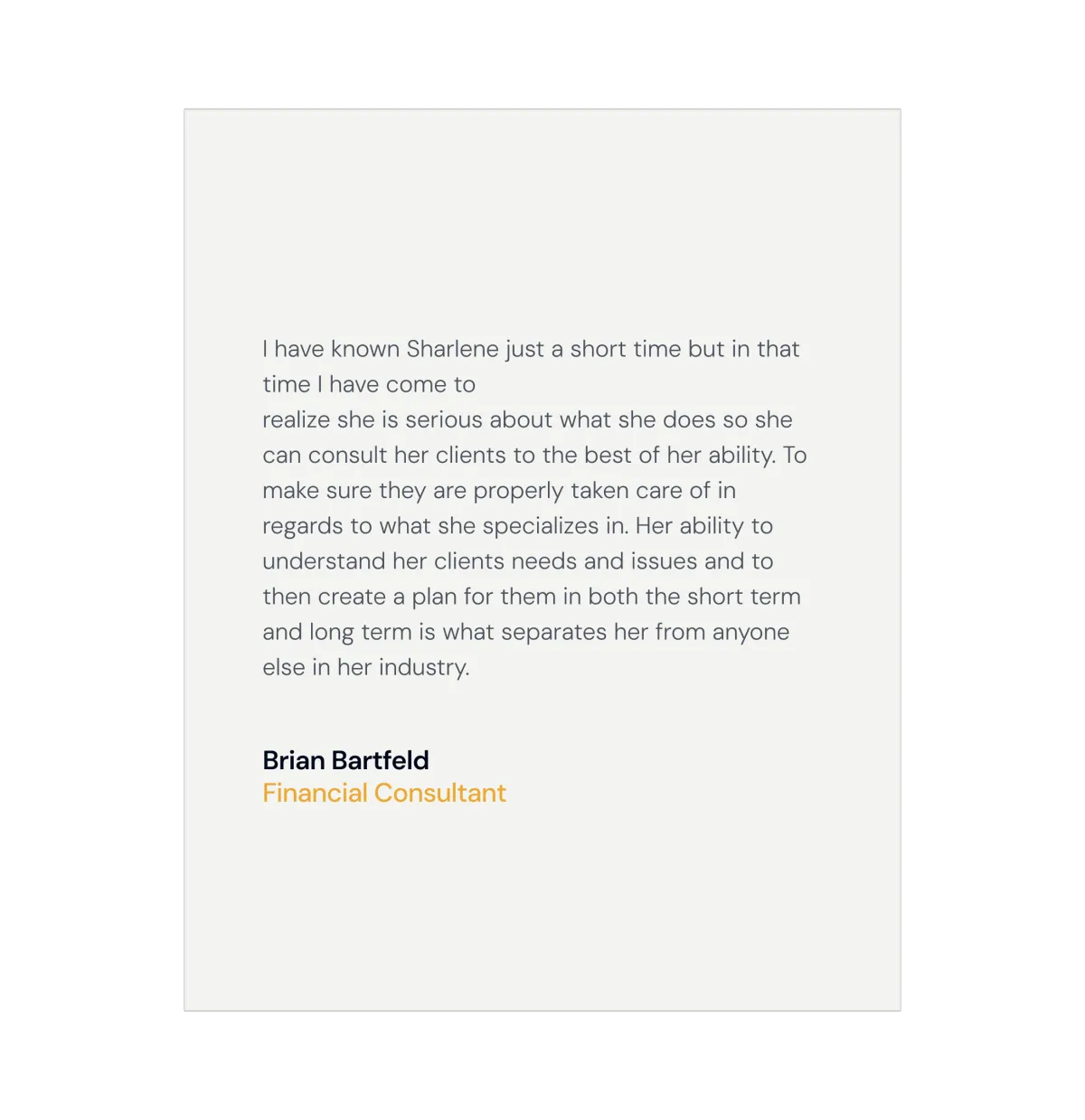

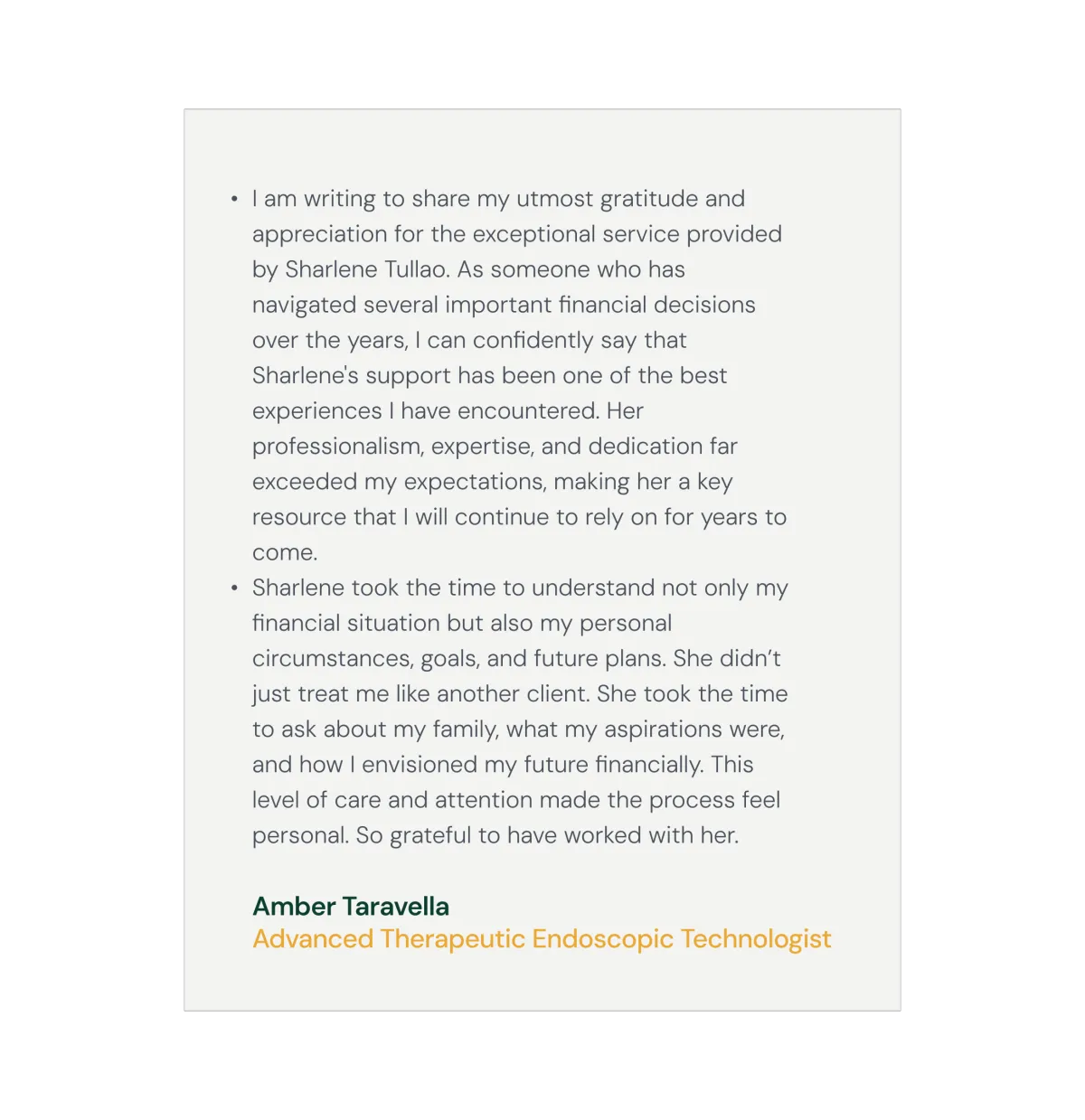

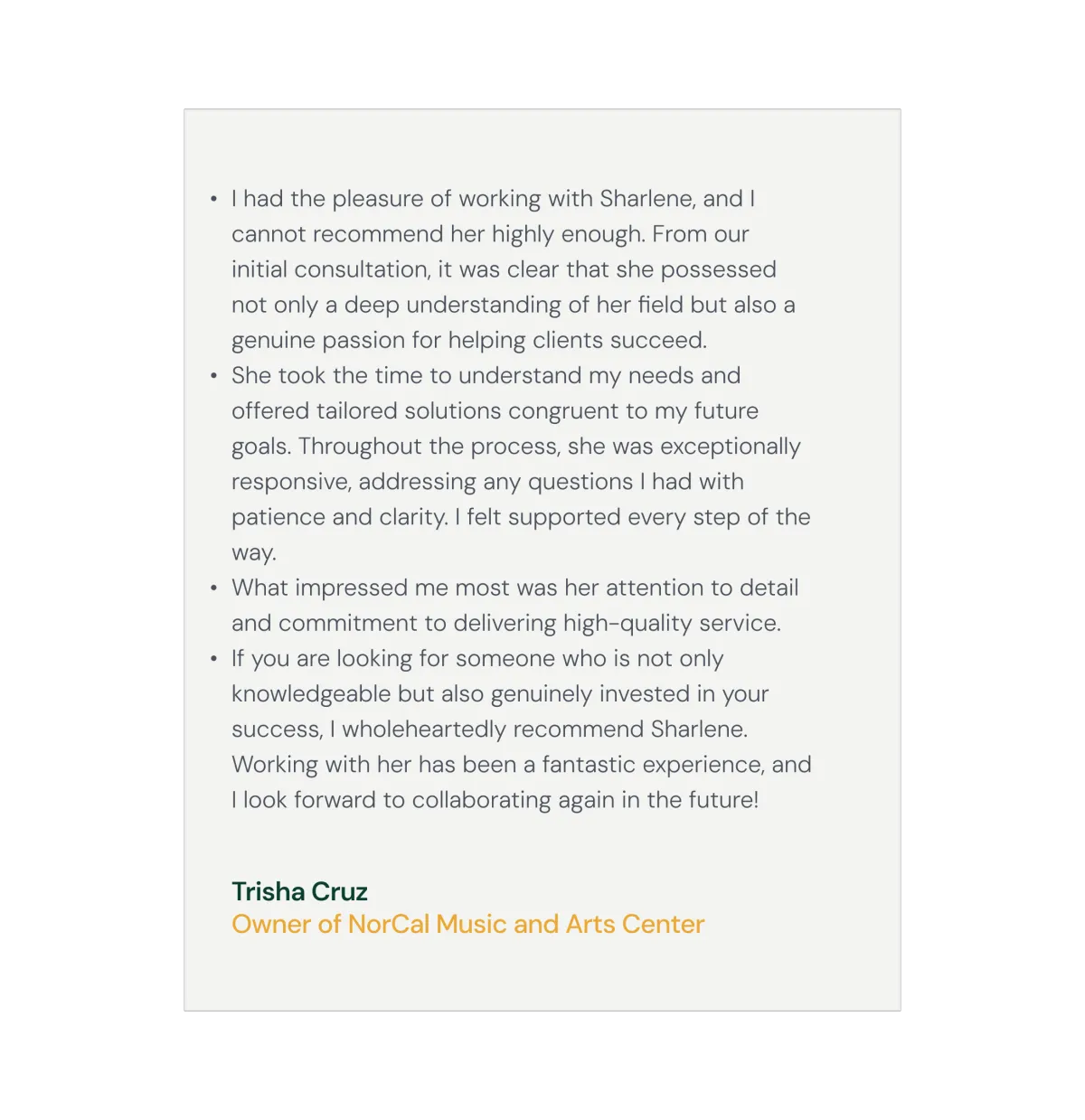

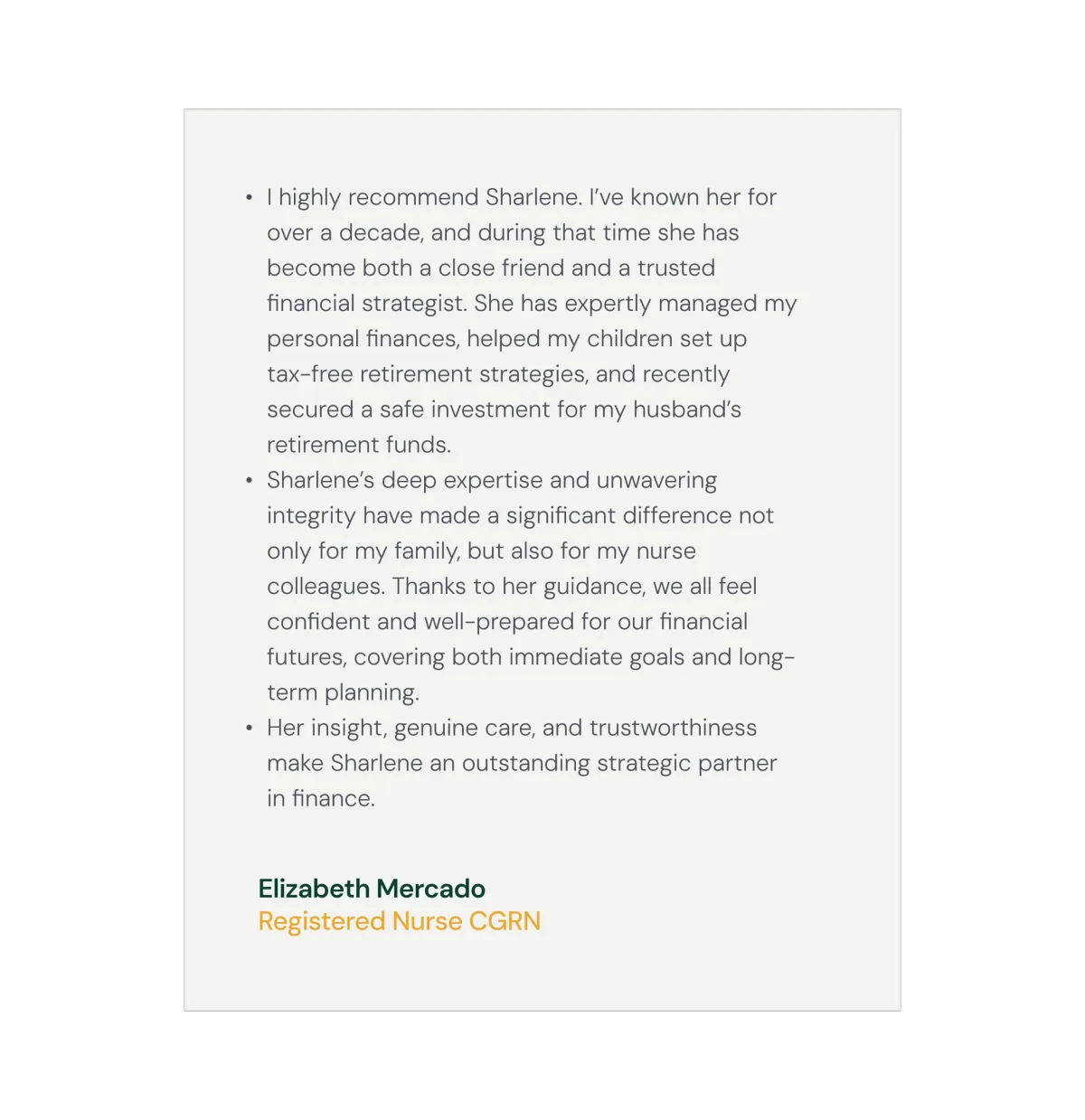

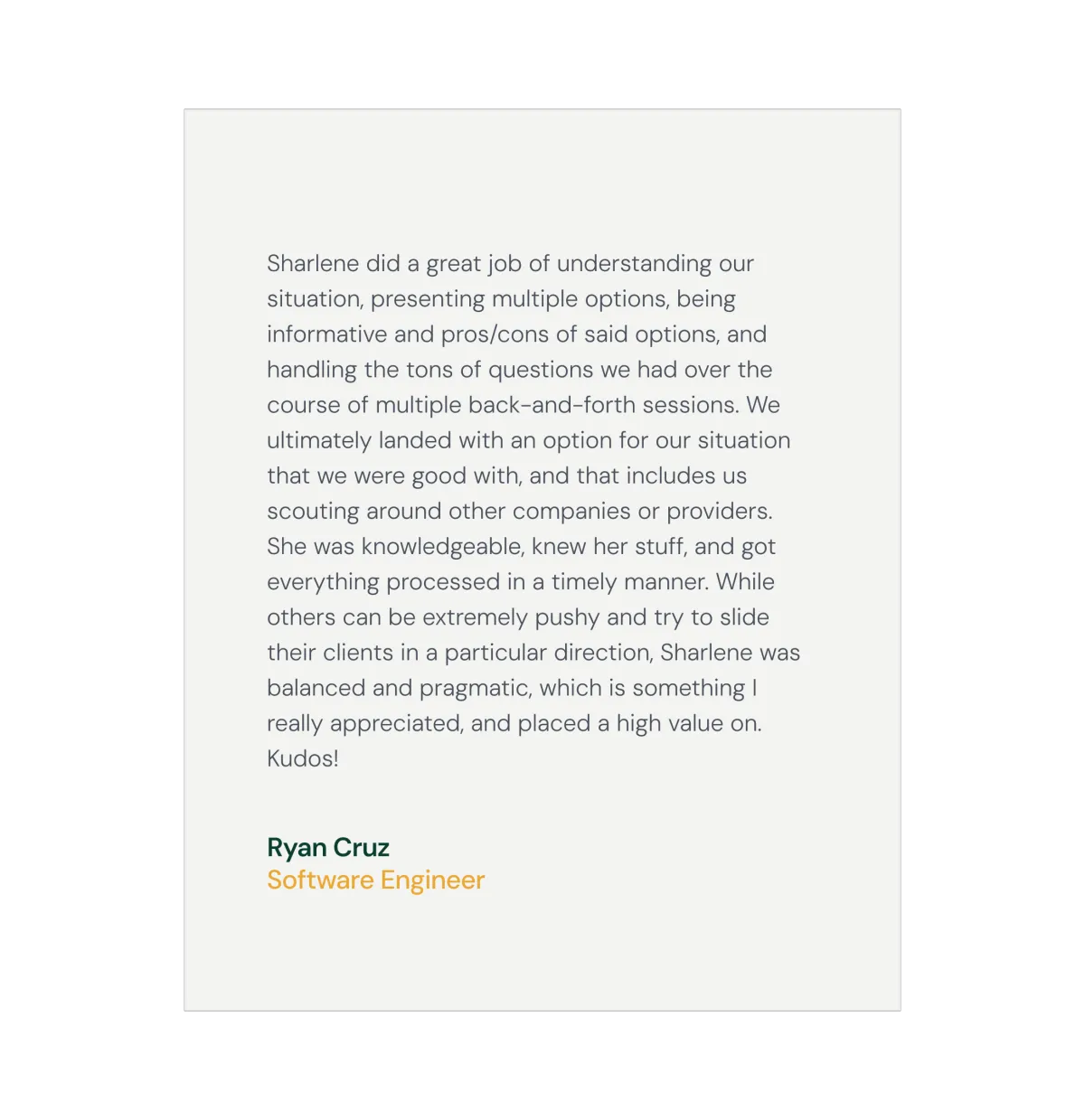

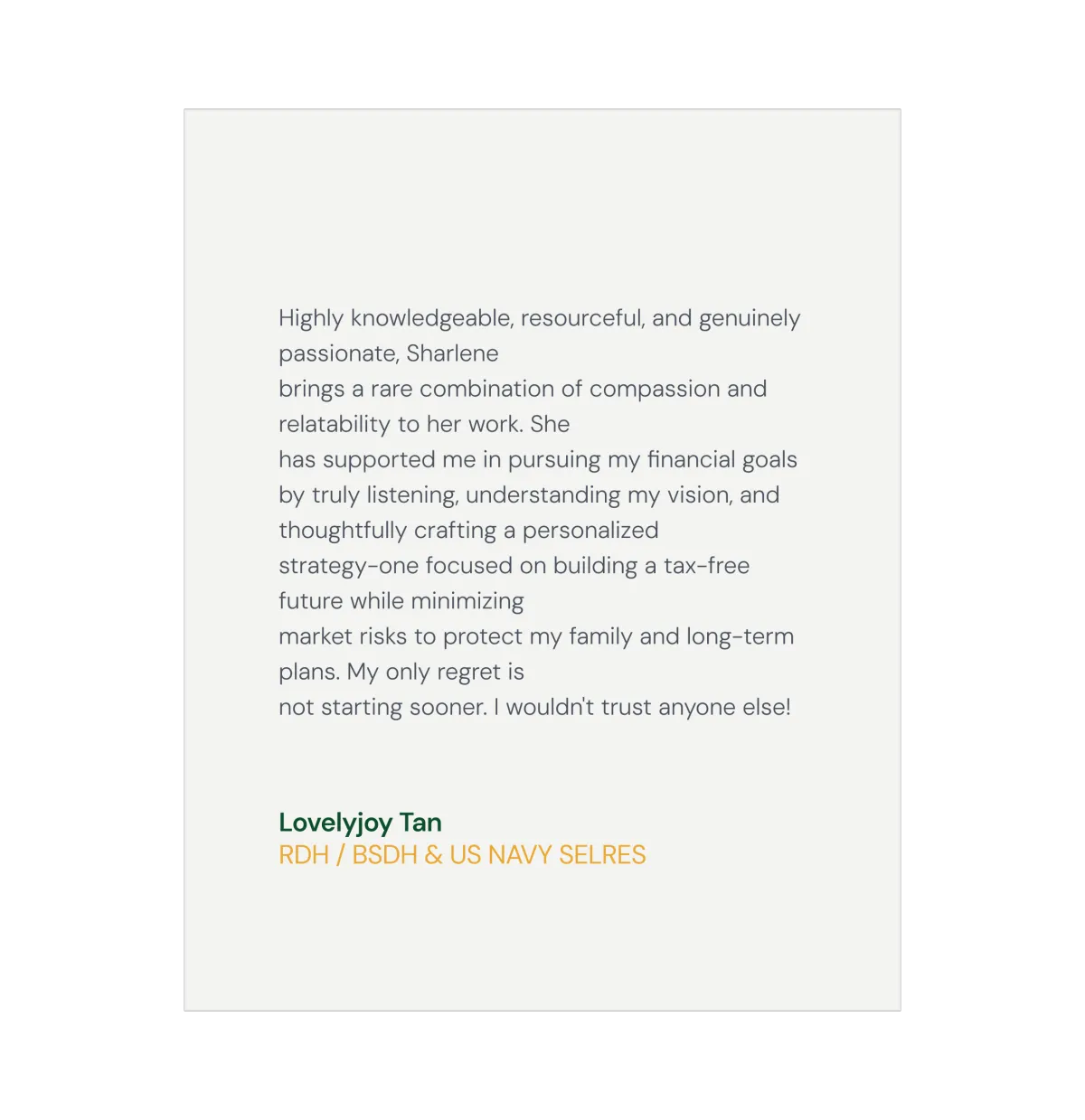

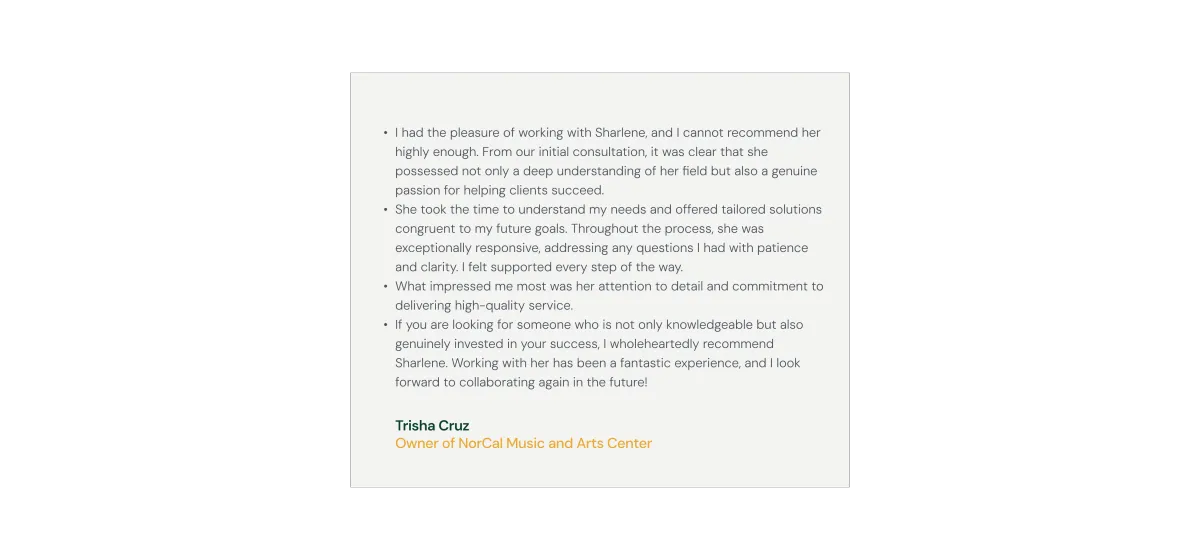

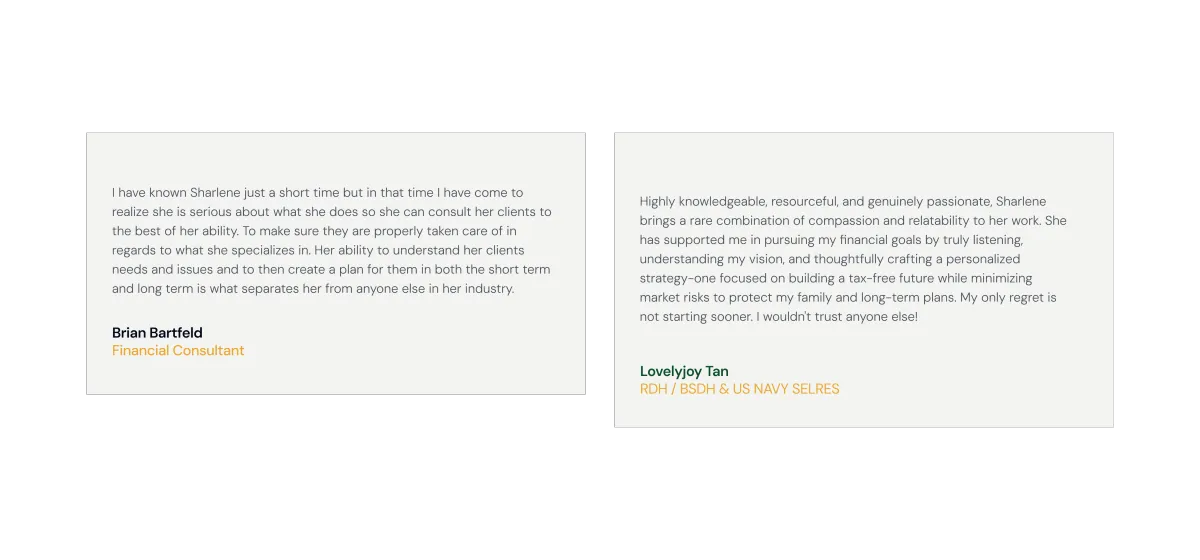

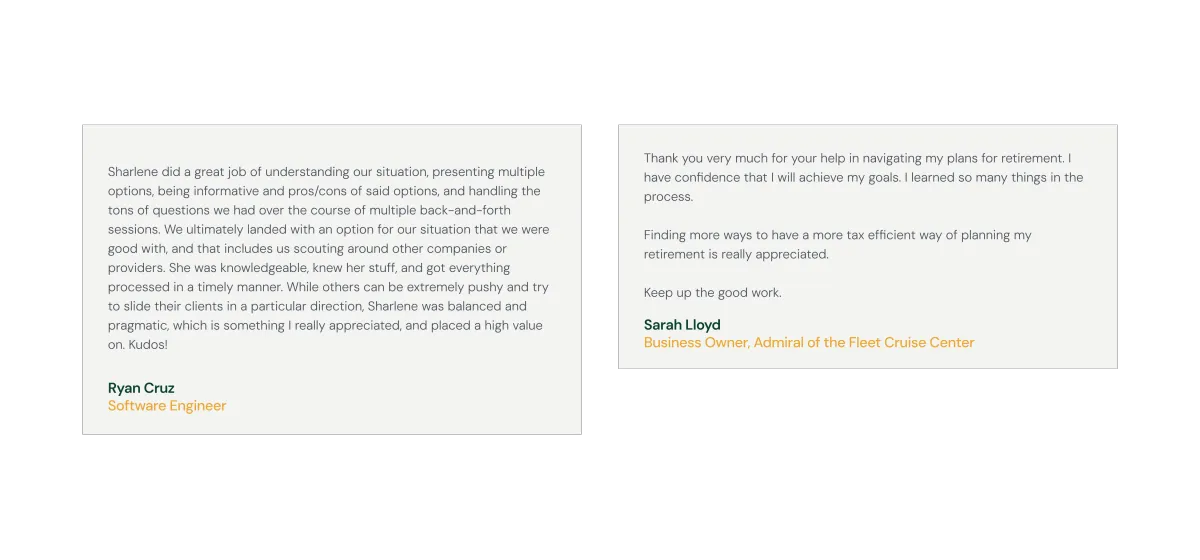

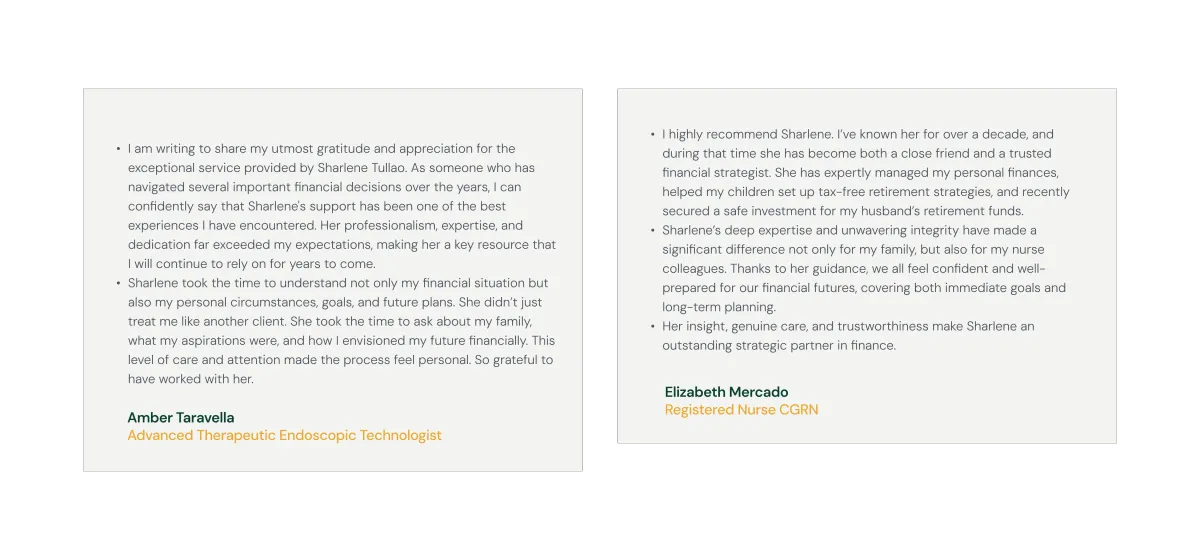

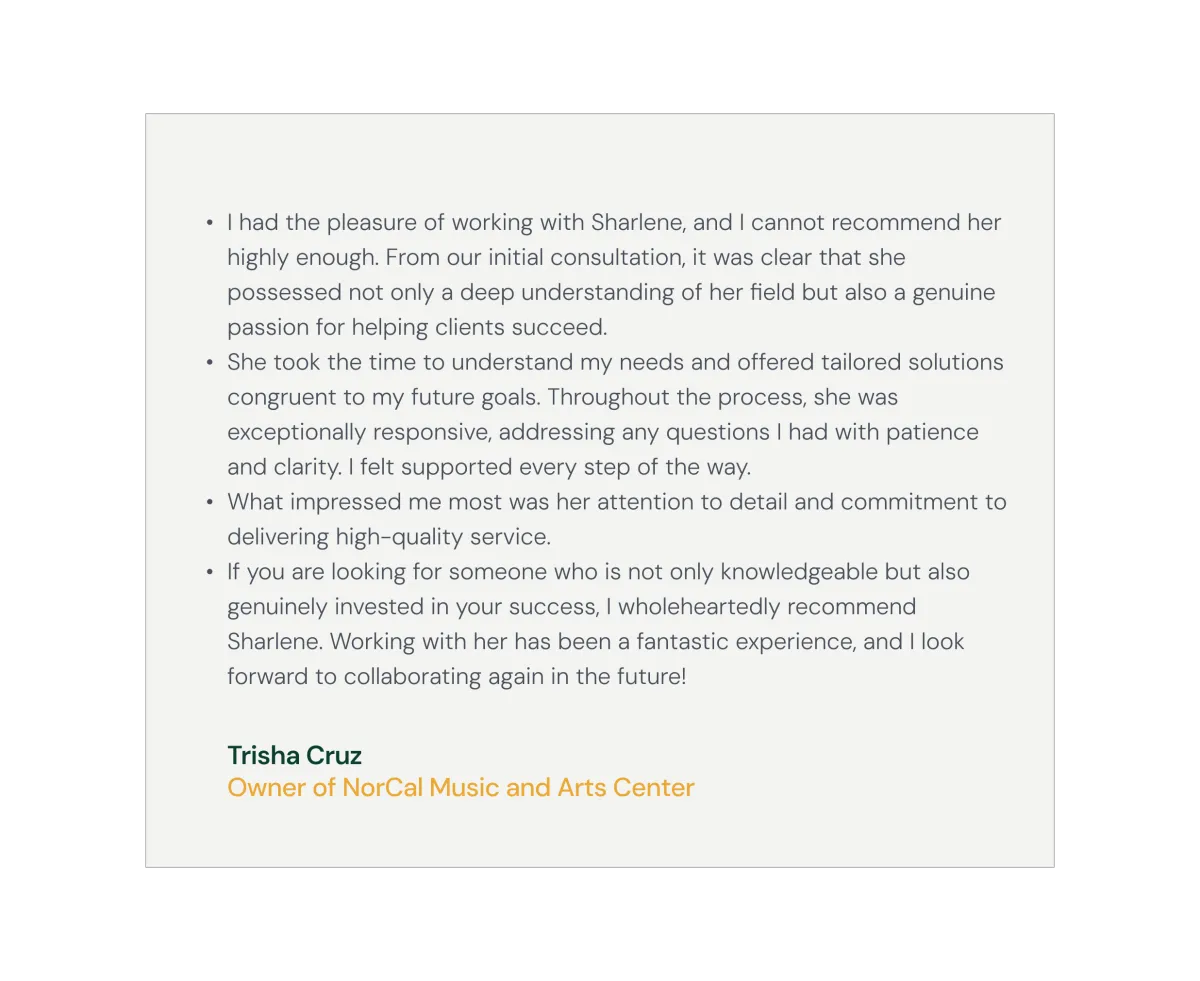

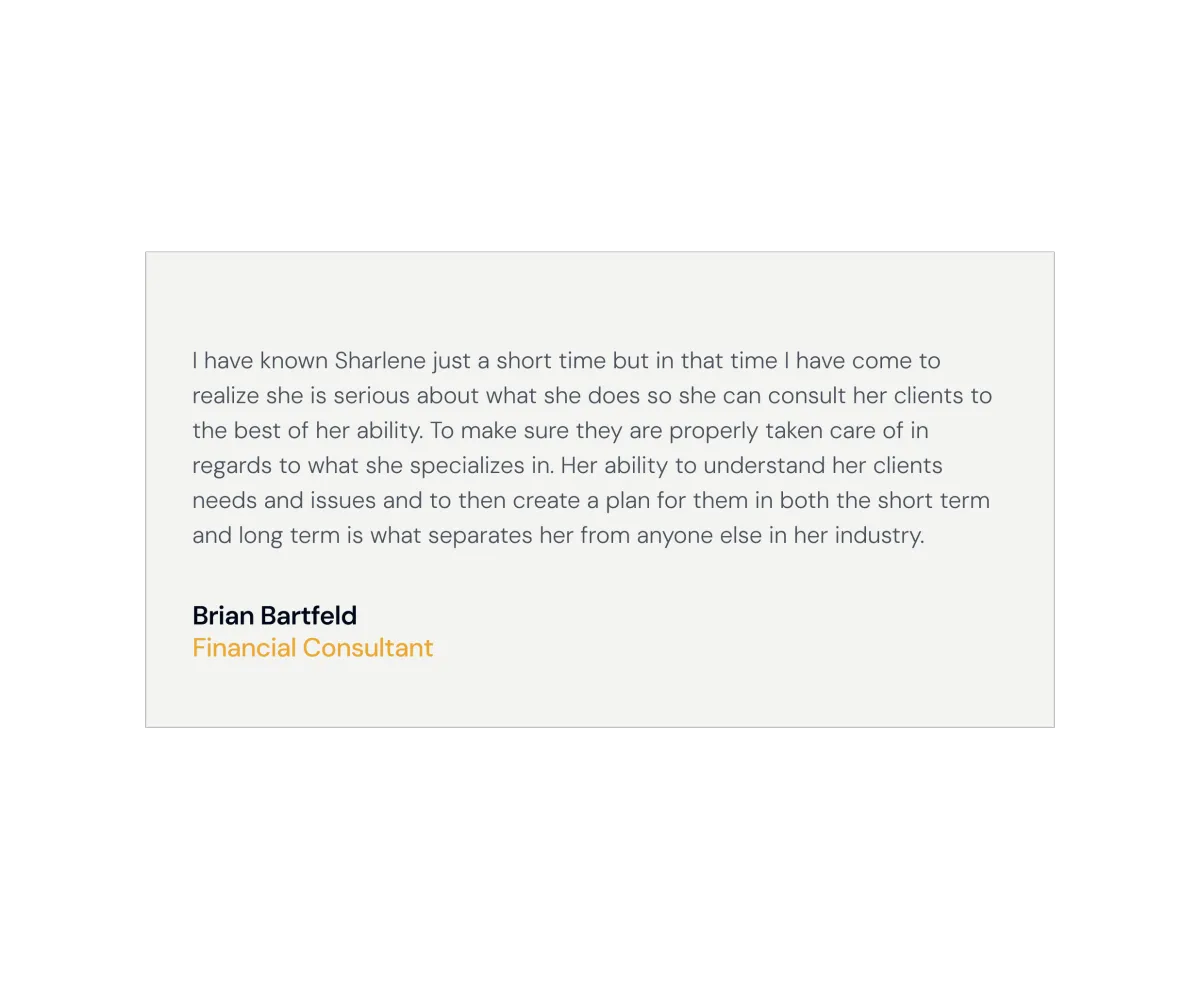

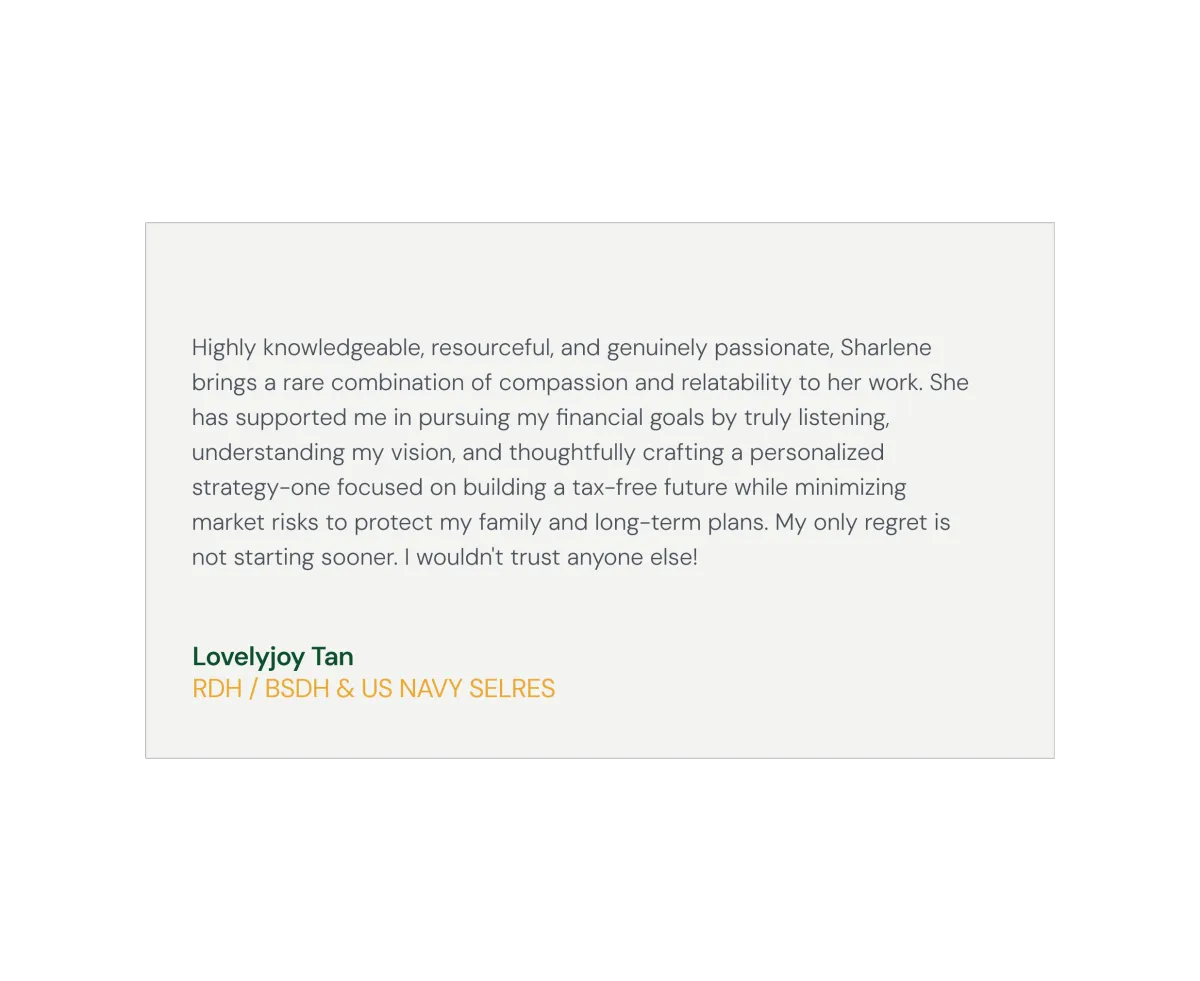

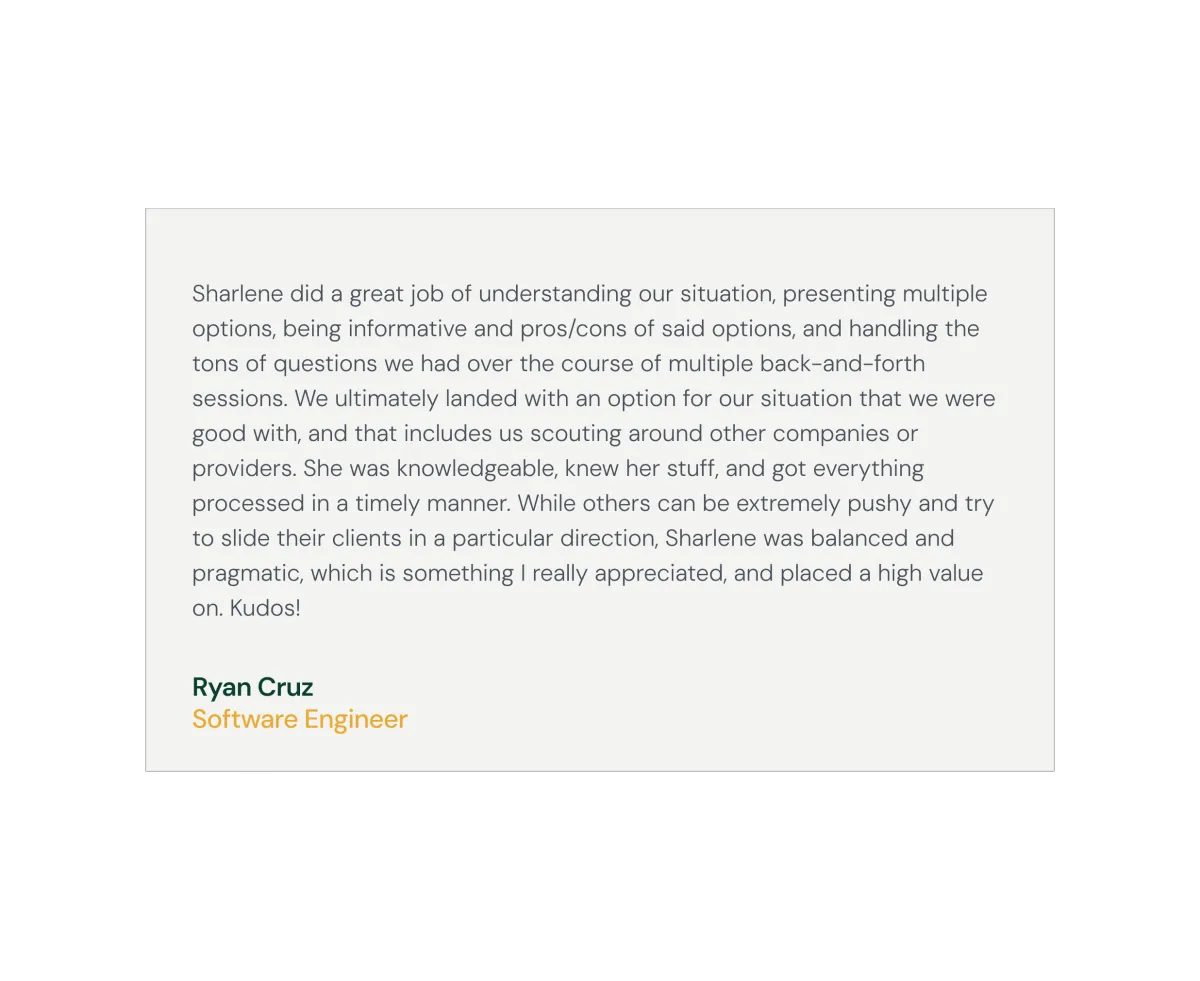

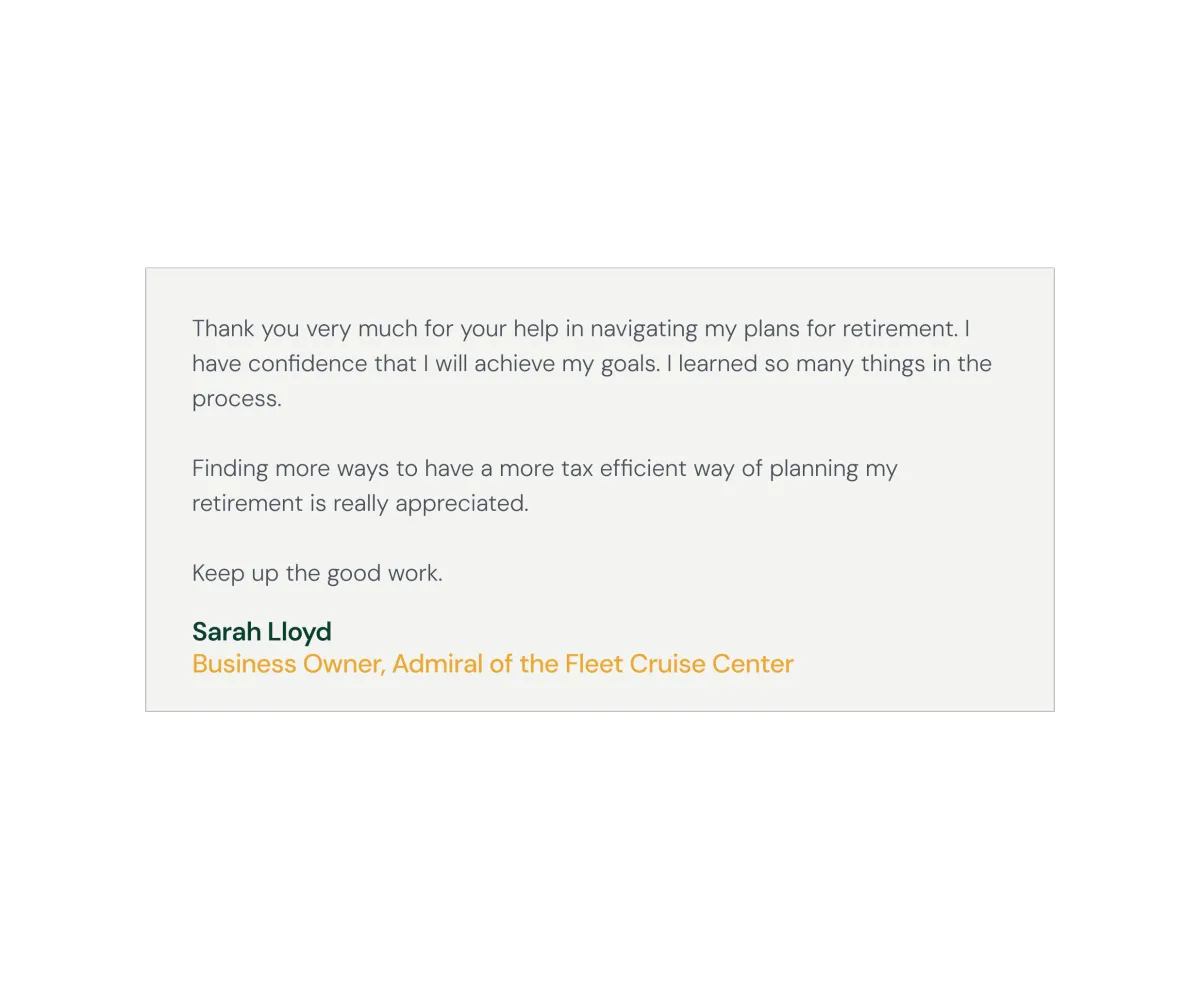

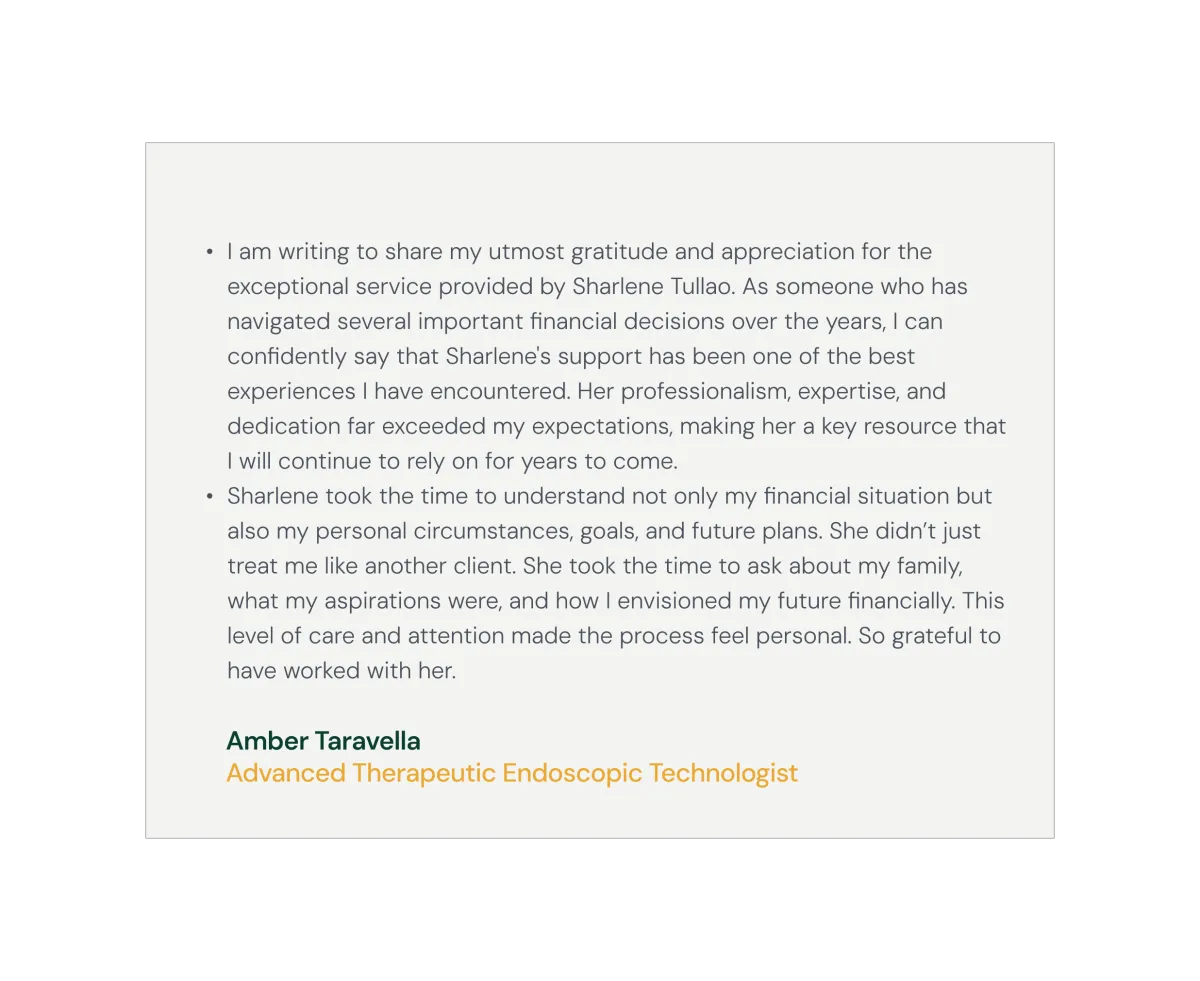

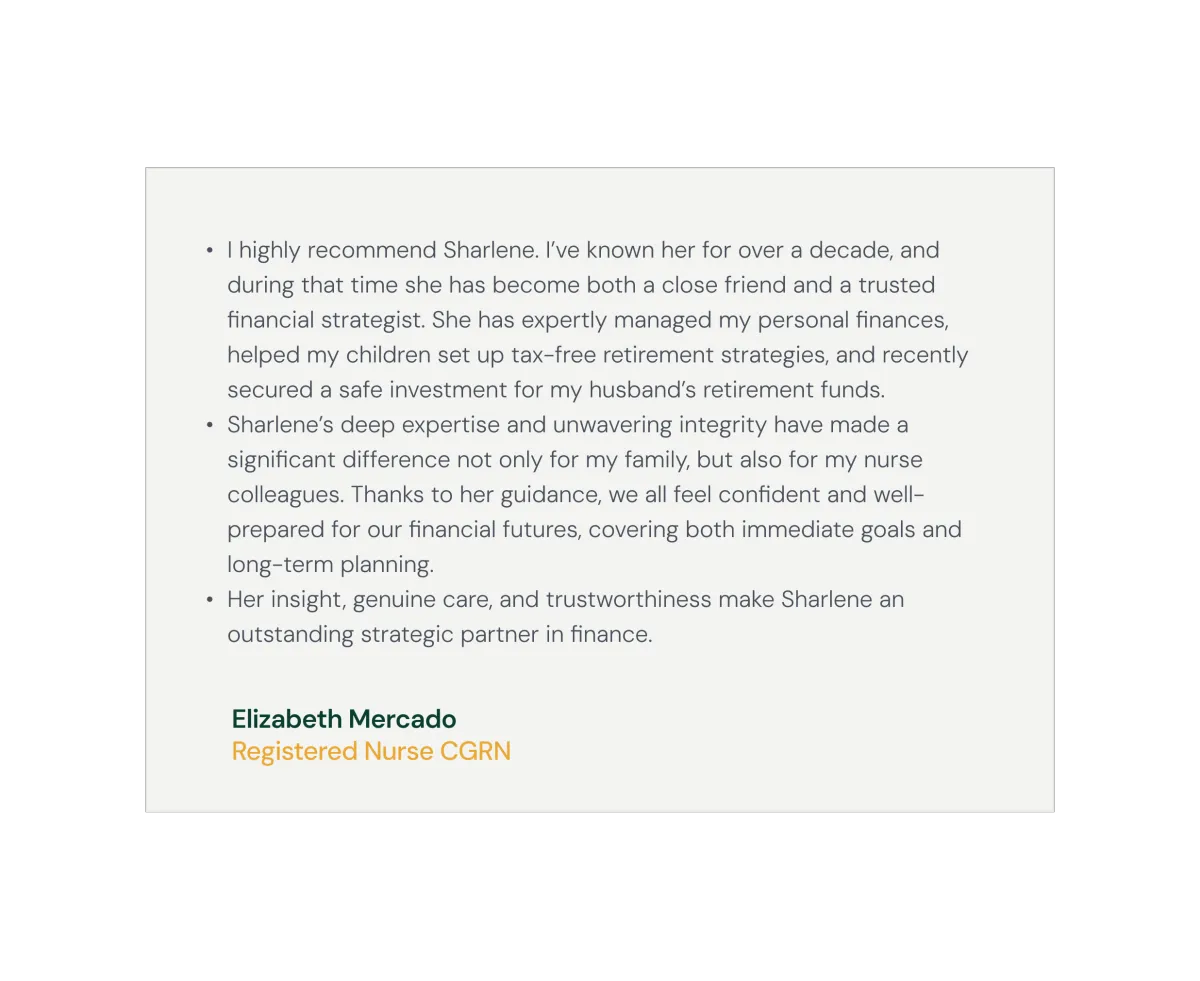

Testimonials

Hear how real clients are creating real change—with clarity, confidence, and smart strategies.

Contact Us

Transforming Financial Challenges into Opportunities for Generational Change.

Frequently Asked Questions

Is this really tax-free, or is that just a marketing term?

Yes — when structured properly, these strategies follow IRS rules that allow your money to grow and be accessed 100% tax-free. We don't bend the rules — we simply use tools the wealthy have relied on for decades, made available to everyday families.

I already have a 401(k). Why would I need something else?

A 401(k) is tax-deferred, not tax-free — which means you'll pay taxes later, potentially at higher rates. You also don't want to gamble your retirement to the volatility of the market. Our strategy helps you diversify your tax exposure, reduce future tax risk, access your money without penalties or age restrictions, and protect your principal.

What kind of results can I expect?

Everyone’s results vary based on age, contributions, and goals — but our clients often see 30–40% more capital preserved by avoiding unnecessary taxes, fees, and market losses. We walk you through real projections based on your specific numbers.

Is this safe? What’s the risk?

Yes — our strategies prioritize principal protection. That means your money isn’t exposed to market downturns. You’ll never lose a dime due to a stock market crash, and your plan is designed for long-term stability and control.

Is there a fee to work with you?

Our guiding principle is to eliminate risks, fees and taxes. We want to stay true to who we are and that's why we don't charge any fees.

I already have a Financial Advisor?

That's great. But we specialize on the Tax-Free side of finance. We specialize in helping people (Eliminate Risk, Fees & Taxes). A typical advisor, if you think about it, actually does the complete opposite. They actually Add Risk, they Add Fees, & they Add Taxes simply based on their specific focus. We’re all in the same industry, but just a very different focus and specialty.

How do I get started?

Just book a free 15-minute call. We’ll go over your current setup, your goals, and let's see if this can even apply to you.

© 2025 All Right Reserved by Sharlene Tullao.